Imagine Ali is buying a car. At the bank, he’s offered two paths: a loan or credit.

A loan gives Ali the full amount upfront to buy the car, which he pays back in steady monthly installments. Credit, on the other hand, is like a safety net—he can borrow exactly what he needs, up to a limit, whenever he wants. Same goal, but two very different ways to get there.

Consequently, understanding the difference between loan and credit plays a key role in making smart financial decisions, whether for personal use, business, or investment. Many people confuse these terms, yet knowing how loan and credit operate can save money, avoid unnecessary debt, and improve financial planning. In this article, we will explore the distinctions, applications, and nuances of these two essential financial tools.

Pronunciation:

- Loan: /loʊn/ (US), /ləʊn/ (UK)

- Credit: /ˈkrɛdɪt/ (US & UK)

Now that we have an overview, let us further explore the difference between loan and credit, and understand why it is important in daily life.

Key Difference Between Loan and Credit

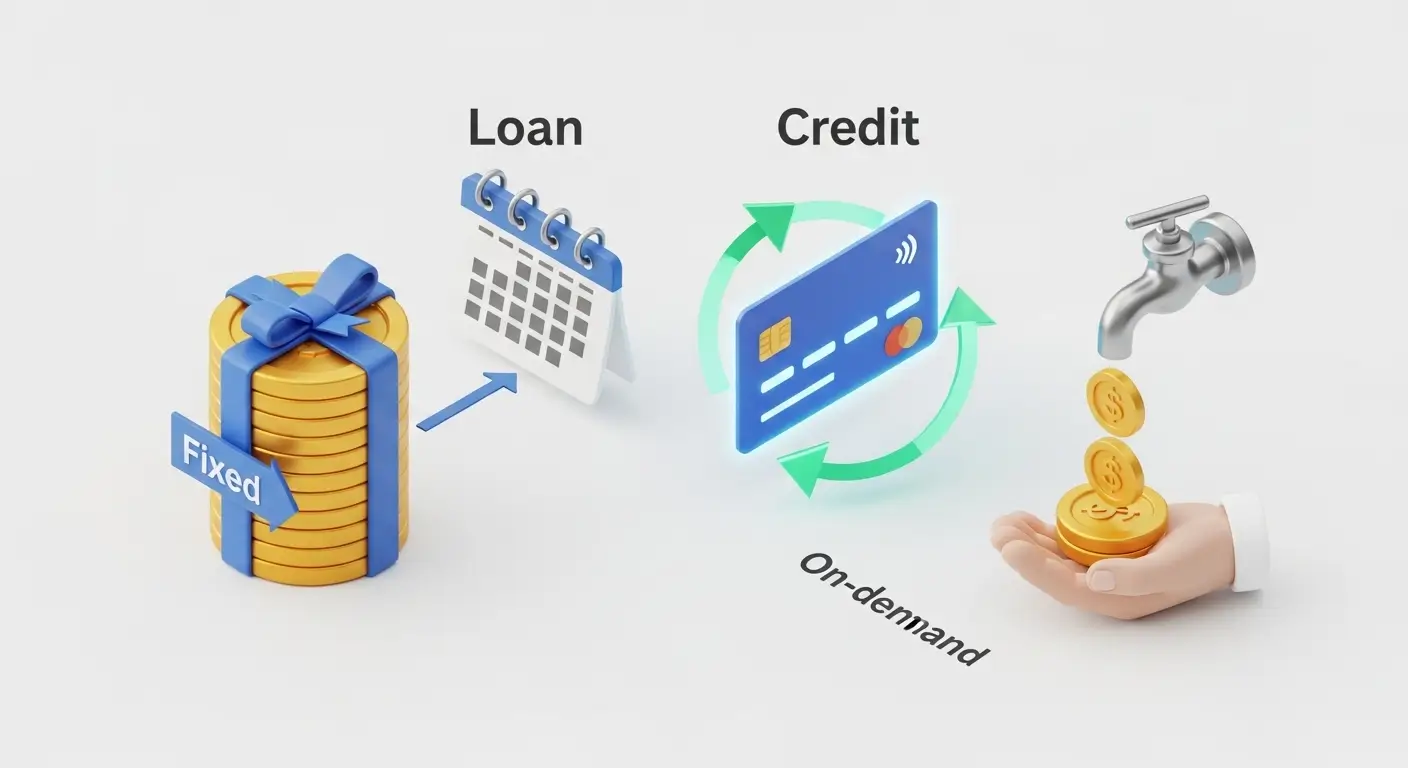

The difference between loan and credit lies mainly in structure, flexibility, and usage. A loan is usually a fixed sum with a defined repayment schedule, whereas credit is a flexible borrowing facility where funds can be drawn and repaid repeatedly up to a limit.

Why Knowing Their Difference Is Important

Understanding the distinction is essential for both learners and financial experts. Loans and credit affect individuals, businesses, and the economy differently. Misunderstanding them can lead to mismanagement of funds, high-interest payments, or missed opportunities. In society, these tools help people invest in homes, start businesses, and meet urgent financial needs. Recognizing their differences ensures responsible borrowing, efficient resource allocation, and stronger financial literacy.

Difference Between the Keywords

Here are 10 key differences between loan and credit, explained with examples:

Definition

- Loan: A lump sum borrowed from a lender to be repaid with interest over time.

- Example: Sara takes a $10,000 car loan from the bank.

- Example: A student loan of $20,000 helps John pay for tuition.

- Credit: A flexible amount of money available to borrow up to a limit.

- Example: Ali has a $5,000 credit card limit for emergencies.

- Example: A business line of credit of $50,000 is used as needed.

Repayment Schedule

- Loan: Fixed installments with set deadlines.

- Example: Monthly mortgage payments of $1,200.

- Example: Personal loan repaid in 36 equal installments.

- Credit: Flexible repayment, borrower can pay any amount within limit.

- Example: Minimum credit card payment of $50 each month.

- Example: Borrowing $2,000 now and $1,000 later within a $5,000 credit limit.

Interest Calculation

- Loan: Interest is calculated on the total borrowed amount.

- Credit: Interest is calculated only on the amount used, not the full limit.

Purpose

- Loan: Often used for a specific purpose (home, education, car).

- Credit: Can be used for various purposes as needed.

Flexibility

- Loan: Fixed, cannot borrow more without applying for a new loan.

- Credit: Reusable as funds are repaid.

Approval Process

- Loan: Requires detailed verification and documentation.

- Credit: Usually quicker, often pre-approved based on creditworthiness.

Collateral Requirement

- Loan: May require collateral (secured loans).

- Credit: Often unsecured, especially for credit cards.

Loan Tenure

- Loan: Typically medium to long-term (1–30 years).

- Credit: Usually short-term, renewable, flexible tenure.

Usage Behavior

- Loan: Encourages disciplined use due to fixed repayment.

- Credit: Can lead to impulsive spending if mismanaged.

Risk Factor

- Loan: Lower risk if repayment is planned.

- Credit: Higher risk of overspending and accumulating debt.

Nature and Behaviour

- Loan: Structured, predictable, and goal-oriented. Borrowers often plan repayment carefully.

- Credit: Flexible, spontaneous, and revolving. Borrowers may use it multiple times for various needs.

Why People Are Confused

Many confuse loan and credit because both involve borrowing money and paying interest. The similarity in terminology and the overlap in usage (like credit cards for large purchases) adds to the confusion. Awareness of structure, repayment, and flexibility clears this misunderstanding.

Difference and Similarity Table

| Feature | Loan | Credit | Similarity |

| Amount | Fixed | Flexible | Both involve borrowing money |

| Repayment | Fixed installments | Flexible | Interest applies |

| Interest Calculation | On full amount | On used amount | Both can affect credit score |

| Purpose | Specific | Any purpose | Both are financial tools |

| Tenure | Medium to long-term | Short-term or revolving | Require lender approval |

| Collateral | Sometimes required | Usually not required | Can impact finances |

| Risk | Lower if managed | Higher if mismanaged | Both involve responsibility |

| Flexibility | Low | High | Both can aid personal/business needs |

Which Is Better in What Situation?

- Loan: Best for large, planned expenses like buying a home, funding education, or investing in business equipment. Fixed terms allow careful budgeting.

- Credit: Ideal for emergencies, short-term needs, or ongoing purchases like groceries, fuel, or temporary cash flow issues. Flexible repayment helps manage unexpected expenses.

Metaphors and Similes

- Loan: “A loan is a sturdy bridge—it helps you cross a big financial gap when you’re planning for the other side.”

- Credit: “Credit is like a water tap—turn it on when you need a drop, but don’t leave it running or you’ll get flooded.”

Connotative Meanings

- Loan: Neutral to positive associated with growth, opportunity.

- Example: Taking a loan to start a small business.

- Credit: Neutral can be positive (flexibility) or negative (debt trap).

- Example: Credit misuse can lead to financial stress.

Idioms / Proverbs

- For instance, the famous saying goes: ‘Neither a borrower nor a lender be. Shakespeare, Hamlet.

- Credit: “Give credit where it’s due.” Recognizing achievement.

Works in Literature

- Loan: The Loan Shark (Novel, Tim Tully, 2014)

- Credit: Credit Where Credit’s Due (Short Story, Sandra Brown, 2007)

Movies

- Loan: Loan Shark (1952, USA)

- Credit: Creditors (1988, Sweden)

FAQs

- Is a loan the same as credit?

No, loans are fixed sums; credit is flexible. - Which is safer to use?

In fact, loans are safer when repayments are carefully planned. - Can credit be converted into a loan?

Yes, some lenders offer balance transfers or fixed-term credit loans. - Do both affect credit score?

Yes, proper use of both improves credit rating. - Which is better for emergencies?

Moreover, credit offers advantages because of its flexibility and immediate access.

How Both Are Useful for Surroundings

Loans and credit stimulate economic growth, support businesses, and allow people to manage personal finances. They create employment, improve living standards, and contribute to financial stability in society.

Final Words

Understanding the difference between loan and credit helps in making informed decisions, planning budgets, and avoiding unnecessary debt. Both tools are indispensable in modern financial life.

Conclusion

While loan and credit might seem similar, in reality, they serve different purposes. Loans are fixed, structured, and goal-oriented, ideal for planned expenditures. Credit is flexible, revolving, and convenient, suitable for emergencies and short-term needs.

Knowing the distinctions enhances financial literacy, promotes responsible borrowing, and empowers individuals to optimize resources effectively. By understanding these differences, learners, professionals, and everyday borrowers can manage finances with confidence, avoid pitfalls, and leverage these tools for personal and societal growth.

Daniel Carter is a research writer and comparison specialist at Compadiff. He focuses on breaking down complex topics into simple explanations so readers can clearly understand the differences between similar concepts, products, and ideas.